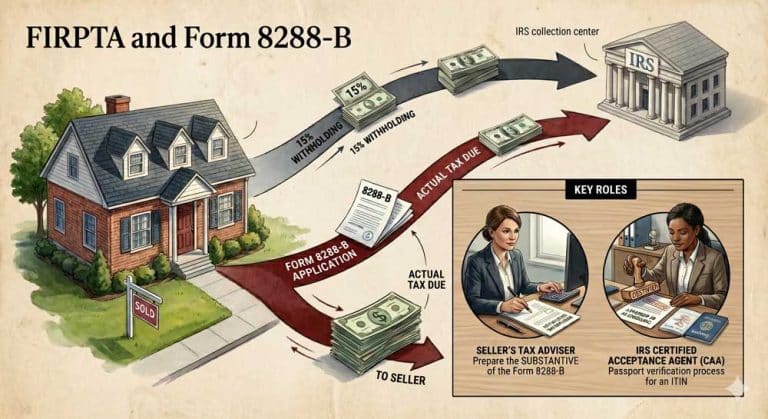

Selling a US property as a foreign owner usually triggers FIRPTA — the Foreign Investment in Real Property Tax Act. Under the default rule, the buyer (the withholding agent) holds back 15% of the gross sale price and sends it to the IRS. That figure has nothing to do with the actual tax owed on the sale. In many transactions the real tax bill is far smaller, sometimes nil. Form 8288-B is the IRS application that brings the withholding back in line with reality. Used correctly, it can release tens of thousands of dollars that would otherwise sit with the IRS for the better part of a year.

What Form 8288-B Actually Does

Form 8288-B is the Application for Withholding Certificate for Dispositions by Foreign Persons of U.S. Real Property Interests. It asks the IRS to either reduce or eliminate the 15% withholding before the money leaves escrow. A withholding certificate is granted in three principal situations: where the seller’s actual federal tax liability on the sale is less than the standard withholding, where the seller is exempt from US tax on the gain under the Internal Revenue Code, or where there is an agreement in place that secures payment of the tax due. The application is reviewed at the IRS service centre in Ogden, Utah.

Who Prepares Form 8288-B

The form is signed by the transferor (seller) or the transferee (buyer) — either party has standing to apply. In practice the seller almost always drives the matter forward, because the seller is the one whose money is sitting in escrow. Either signature is technically valid; the buyer simply rarely has the incentive to do the work.

A foreign seller without US tax expertise should not attempt the form alone. The application requires a precise calculation of estimated gain, supporting closing-cost evidence, original cost basis records, depreciation schedules where the property was rented, and a clean explanation of the legal category being claimed. In a typical FIRPTA closing, responsibilities tend to fall as follows:

- The escrow or title company holds the funds, files Forms 8288 and 8288-A after closing, and remits the withholding to the IRS via EFTPS. Note that paper checks are no longer accepted, with all FIRPTA payments required to flow through EFTPS as of 30 September 2025 — a change confirmed by industry guidance from major US title insurers including Stewart Title.

- The closing attorney or real estate counsel confirms whether the seller is in fact a foreign person, drafts the FIRPTA affidavits, and reviews the 8288-B before submission.

- The tax practitioner or prepares the substantive 8288-B calculation, attaches the supporting schedule, and tracks the matter with the IRS.

- The IRS U.S. Tax Service handles the ITIN application that runs alongside the 8288-B for any seller who does not yet hold a US Tax ID.

Most escrow officers will tell sellers plainly that Form 8288-B sits outside their scope. Their role is the closing and the post-closing remittance; the application for reduced withholding belongs with the seller’s tax adviser.

When to Prepare and File

Timing is the part that most sellers get wrong. The application must reach the IRS on or before the date of transfer. Once the property has changed hands, the chance of avoiding the standard 15% withholding shrinks considerably. The IRS aims to act on the application within about ninety days, but real-world processing has been running longer than that. As long as the application is pending on the closing date, the withholding stays in escrow rather than being remitted to the IRS — the buyer must still withhold, but the funds sit until the IRS issues either an approved certificate or a denial.

Settled industry practice from the FIRPTA-specialist firms is to begin the file three to four months ahead of the planned closing. That window gives time for the ITIN to be issued where it is needed, for the calculation to be checked, and for any IRS follow-up correspondence to be answered without throwing off the closing schedule.

The ITIN Connection — and Why a U.S. Tax Service Matters

Form 8288-B requires the US Taxpayer Identification Number of every transferor and transferee. A foreign individual who has never filed a US return will not have an SSN, and almost certainly will not have an ITIN. Without a TIN, two things happen: the 8288-B cannot be approved, and the IRS will not stamp Form 8288-A Copy B, which is the document the seller later needs in order to claim the withheld amount as a credit on a 1040-NR return.

The fix is to apply for the ITIN at the same time the 8288-B is filed. Form W-7 is attached to the 8288-B, and the package goes to the IRS together.

This is where the IRS U.S. Tax Service earns the fee. A CAA is authorised by the IRS to:

- Verify the seller’s passport in person or by secure video interview, so the original passport never has to leave the seller’s hands or be mailed to Austin, Texas.

- Complete Form W-7 with the agent codes and the correct exception (Exception 4 covers FIRPTA dispositions).

- Issue the Certificate of Accuracy (Form W-7 COA) that travels with the file.

- Resolve CP566 or CP567 ITIN rejection notices where they arise, often without a fresh fee.

Foreign sellers in the United Kingdom, the UAE, Saudi Arabia, Singapore, India, and other markets routinely use a U.S. Tax Service for one practical reason: it removes the well-known risk of an original passport going missing in international post.

Common FAQs

Does the US-UK tax treaty eliminate FIRPTA?

No. The treaty does not exempt gain on US real estate. A Form 8288-B remains the right tool to reduce the withholding to the tax actually due.

The buyer says they will use the property as a residence — does the 15% drop?

Possibly. Where the buyer signs an affidavit confirming intended personal residence and the sale price is at or below $300,000, FIRPTA withholding can be reduced to zero. Between $300,001 and $1,000,000, the rate drops to 10% on the same personal-residence basis. Above $1,000,000 the rate stays at 15% regardless of the buyer’s intent. The fuller list of FIRPTA exceptions and their conditions is worth reviewing before signing the contract.

Can the application be filed after closing?

Late filings are accepted in narrow circumstances, but by that point the buyer has usually already remitted the 15% to the IRS within the twenty-day window. The remedy then shifts from withholding reduction to a refund claim on Form 1040-NR using the stamped Form 8288-A.

How long does the ITIN itself take?

The IRS publishes about seven weeks. In practice, eleven to twelve weeks has been more common, longer during peak filing season. This is a meaningful reason to begin the 8288-B and ITIN package early.

Is Form 8288-B the same as Form 8288 or 8288-A?

No. Form 8288 and Form 8288-A are filed by the buyer after closing to report and pay the withholding. Form 8288-B is filed before closing by either party to ask the IRS for a smaller withholding figure. The three forms are part of the same FIRPTA framework but serve different purposes at different stages.

Closing Thoughts

Form 8288-B is straightforward in principle and unforgiving in practice. The two failure points are timing and the ITIN. Both are avoidable with a tax adviser who runs FIRPTA files routinely and a U.S. Tax Service who can certify the seller’s passport without it leaving the seller’s hand. A correctly prepared 8288-B, filed before closing and supported by a complete Form W-7 package, can return the difference between fifteen percent of the sale price and the actual federal tax on the gain — money that would otherwise sit with the IRS for the better part of a year before any refund is processed.If you are planning to sell a US property and need the 8288-B prepared properly, or you need an ITIN to make a reduced-withholding application possible, our FIRPTA and U.S. Tax Service team can take the file from passport certification through to the post-sale refund claim. Engagements are handled remotely for clients in the UK, Europe, the Middle East, Asia, and elsewhere.