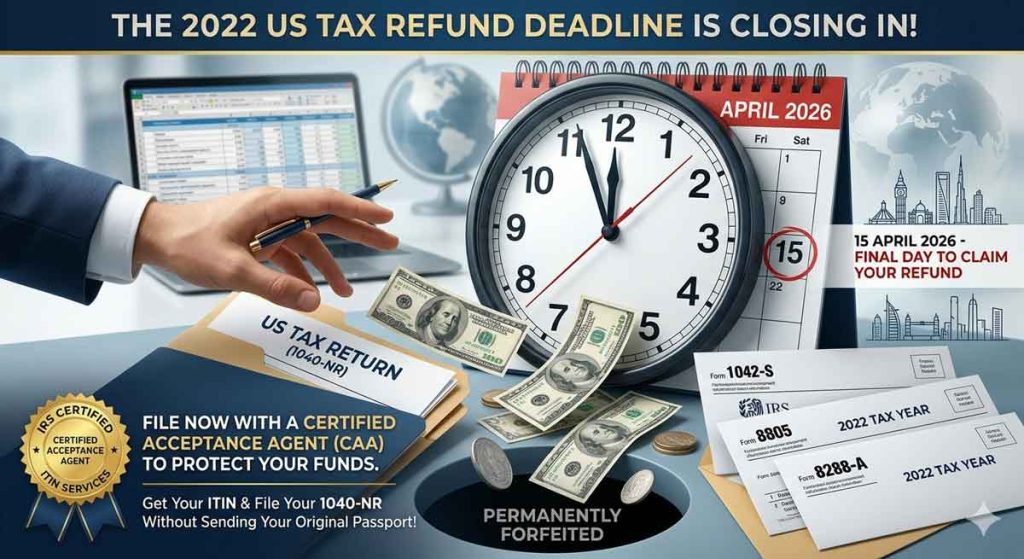

Most people assume that if the IRS owes them money, it will wait. It will not. Under US federal tax law there is a strict three-year statute of limitations on tax refund claims. For the 2022 tax year, that window closes on 15 April 2026. Once that date passes, any unclaimed refund is forfeited permanently — there is no appeal, no grace period, and no exceptions for people who simply did not know.

If you received any of the following forms for 2022 and have not yet filed a US tax return, this is the post you need to read before the deadline arrives.

Which 2022 Tax Forms Could Mean the IRS Is Holding Your Money?

The US withholding system is built to collect tax upfront, typically at the highest possible flat rate, and leave taxpayers to reclaim the excess through a filed return. For foreign nationals, non-resident investors, overseas LLC and LLP partners, and international individuals with any US-sourced income, the forms below are the ones that most commonly carry refundable withholding.

- Form 1042-S — Foreign Person’s US Source Income Subject to Withholding. This applies to investment income, partnership distributions, rental income, scholarship payments, and gambling winnings paid to foreign nationals. The default withholding rate is 30%. In many cases, the correct rate under an applicable tax treaty is considerably lower — sometimes zero.

- Form 1099 / 1099-R — Distributions, interest, dividends, and retirement or pension income. Federal tax may have been withheld at source and may be partially or fully refundable depending on your filing position.

- Form 8805 — Foreign Partner’s Information Statement of Section 1446 Withholding Tax. If you are a non-US partner in a US LLC or LLP, this form reports withholding on your share of partnership income. The withholding rate applied is often 37%, the top US marginal rate, regardless of what you actually owe.

- Form 8288-A — Statement of Withholding on Dispositions by Foreign Persons of US Real Property Interests. Under FIRPTA rules, 15% of the gross sale price is withheld when a foreign person sells US real estate. If the actual gain is lower than 15% of the full price, or if the property sold at a loss, the excess is refundable by filing a 1040-NR tax return.

- Schedule K-1 — Partner’s share of income, deductions, and credits from a US LLC or LLP. Non-resident foreign partners frequently have excess withholding here that can be reclaimed.

- Form W-2G — Gambling winnings from US casinos. Establishments in Las Vegas, Atlantic City, and elsewhere withhold 30% from winnings paid to foreign players. Many countries have a US tax treaty covering gambling income that reduces this rate to zero.

If any of these forms were issued to you for the 2022 tax year and you have not filed, the 15 April 2026 deadline applies to all of them.

Why 15 April 2026 Is the Point of No Return

The three-year refund limitation is set out in Section 6511 of the Internal Revenue Code. It runs from the original due date of the return, not from when you received your forms or became aware of the obligation. For 2022 returns, the original due date was 15 April 2023. Three years from that date is 15 April 2026.

The IRS will not send you a reminder. They will not call. When the deadline passes, they retain the funds legally. The courts have enforced this rule consistently, and there is no statutory provision that allows the IRS to voluntarily process an out-of-time refund claim in ordinary circumstances.

This is not a technicality that clever paperwork can resolve after the fact. It is a hard cut-off. The only way to protect your refund is to file before the date arrives.

For a full overview of US tax filing requirements for foreign nationals and Americans living abroad, the team at Tax and Accounting Hub has put together a comprehensive service guide covering who needs to file and how the process works from outside the US.

Who Is Most Likely Sitting on an Unclaimed 2022 Refund Right Now?

Our team works with clients across the UK, India, the UAE, Singapore, Belgium, Saudi Arabia, Qatar, and beyond. The profiles below represent the situations we see most regularly where significant refundable withholding has gone unclaimed.

Foreign nationals receiving passive income from US investments

If you are a non-US investor receiving dividends, interest, or royalties from US-based stocks, funds, or other instruments, your withholding agent will have issued a Form 1042-S showing 30% withheld. Most countries — including the UK, India, UAE, Germany, France, Netherlands, Singapore, and many others — have an active tax treaty with the US that reduces this rate substantially, in some cases to zero. The excess is recoverable by filing a 1040-NR return. Our post on Form 1042-S withholding and US tax reclaims for foreign nationals explains how this works in practice.

Foreign partners in US LLCs and LLPs

As a non-US member or partner in a US limited liability company or partnership, you will typically receive a Schedule K-1 alongside a Form 8805. The 37% withholding rate applied to your partnership income is based on the top US marginal rate. Once allowable deductions and applicable treaty positions are factored in, the actual liability is almost always lower. Foreign members of US LLCs and LLPs operating from London, Bangalore, Chennai, Dubai, Abu Dhabi, Mumbai, Singapore, or anywhere else internationally often have significant refunds available. See the detailed guide to ITIN applications for foreign persons with US LLC and LLP business income.

Foreign nationals who sold US real estate — FIRPTA withholding

When a foreign person sells US property, FIRPTA rules require the buyer’s agent to withhold 15% of the gross sale price. This is reported on Form 8288-A. If the actual taxable gain is less than 15% of the full sale price — which is common — the difference is refundable. In cases where the property was sold at a loss or below a qualifying threshold, the entire amount may be reclaimable. Form 8288-B can be used to apply for a reduced withholding rate before or at closing, but if that was not done at the time, a 1040-NR return is the route to claiming the refund after the fact. This applies to sellers based in the UK, India, Europe, the Middle East, and anywhere else outside the US.

International visitors who won at a US casino

US casinos withhold 30% from gambling winnings paid to foreign players, reported on Form 1042-S or Form 1099-G. If your country of residence has a US tax treaty covering gambling income — and many do, including the UK — the correct withholding rate may be zero. A 1040-NR return filed before 15 April 2026 allows you to reclaim the excess 30% withheld from your 2022 winnings. Our blog post covering how to reclaim tax on Las Vegas gambling winnings via Form 1042-S walks through the eligibility criteria and process in full.

Non-US YouTubers and digital content creators

Non-US creators earning advertising revenue from US-based viewers are subject to US withholding tax on that income, reported on Form 1042-S. Without a valid Form W-8BEN on file, Google withholds at the full 30% rate. If you received a 1042-S for your YouTube earnings in 2022, you may be entitled to a refund based on your country of residence and the applicable treaty rate. See our article on ITIN applications and 1042-S tax reclaims for YouTubers.

US citizens and green card holders filing jointly with a non-US spouse

A US citizen or resident alien who is married to a foreign national and wishes to file a joint 1040 return using Married Filing Jointly status will need their spouse to have a valid US Tax ID. If the non-US spouse does not have a Social Security Number, they will need to apply for an ITIN using Form W-7 — a process our team handles regularly for clients based in the UK, Europe, India, and the Middle East. This also applies where the foreign spouse is being claimed as a dependent.

UK and international beneficiaries of US estates and 401(k) plans

Foreign nationals who inherit assets from a US estate, receive distributions from a US 401(k) plan, or are named as beneficiaries of a US trust will often have withholding applied to those payments and reported on Form 1042-S or 1099-R. If a 2022 distribution was received with withholding attached and no return has been filed, 15 April 2026 is the deadline to claim it back.

What Filing a 2022 Return Actually Involves

The process depends on your status.

If you are a non-resident alien — not a US citizen, not a green card holder, and not meeting the substantial presence test for 2022 — you file Form 1040-NR, the US Nonresident Alien Income Tax Return. This is the standard return for claiming refunds on Forms 1042-S, 8805, 8288-A, and 1099 income.

If you are a US citizen or green card holder living abroad, you file Form 1040, the standard US Individual Income Tax Return, alongside any applicable foreign earned income exclusion or foreign tax credit forms.

In both cases, if you do not already have a US Taxpayer Identification Number — either a Social Security Number or an Individual Taxpayer Identification Number — you will need to obtain one before or at the same time as filing your return. Without a valid tax ID, the IRS cannot process the return.

Do You Need an ITIN to File and Claim Your Refund?

An ITIN (Individual Taxpayer Identification Number) is a nine-digit tax processing number issued by the IRS to individuals who need to file a US tax return but are not eligible for a Social Security Number. This includes non-resident aliens filing 1040-NR, foreign nationals with US-sourced income, non-US spouses being added to a 1040 return, dependents who are foreign nationals, and beneficiaries of US estates and trusts.

Without a valid ITIN or SSN, the IRS will reject your return. The ITIN application is made using Form W-7 and is typically submitted alongside the tax return itself, with identity documents attached. The most important thing to understand about the document requirements is that the IRS does not accept notarised or apostilled copies of passports. The only accepted certifications are originals or copies certified by an IRS-approved U.S. Tax Service.

If your ITIN was issued before 2013 or covers certain digit ranges issued before 2016, it may have expired and require renewal before it can be used on a filed return. Our ITIN application guide for non-residents and foreign nationals covers both new applications and renewals in detail.

What an IRS U.S. Tax Service Does — and Why It Matters for Your Application

An IRS U.S. Tax Service is an individual or organisation that has entered into a formal written agreement with the Internal Revenue Service authorising them to verify and certify identity documents for ITIN applicants. The CAA designation is the highest level of IRS authorisation for ITIN work, and it carries responsibilities and standards that a standard U.S. Tax Service does not have to meet.

The key distinction between a CAA and a standard U.S. Tax Service (AA) is scope: a standard AA can only certify documents for the primary applicant. A U.S. Tax Service can certify documents for the primary applicant, spouse, and all dependents — which is essential for families or for any situation where multiple ITINs are needed simultaneously, such as a US citizen filing jointly with a non-US spouse and claiming foreign national dependents.

When you work with a CAA, your original passport does not go to the IRS. The CAA reviews the original during a video call or in-person meeting, completes a Certificate of Accuracy (Form W-7 COA), certifies a copy with their agent seal, and submits the full package to the IRS ITIN office. This protects your original documents, reduces processing delays, and substantially lowers the risk of rejection.

Our team operates as IRS-approved U.S. Tax Services with clients in the United Kingdom — including London, Manchester, Birmingham, Edinburgh, Glasgow, Liverpool, Leeds, Bristol, Bedford, Cambridge, and Scotland — as well as in India (Bangalore, Chennai, Mumbai, Delhi, Hyderabad, Pune, and other cities), the UAE (Dubai, Abu Dhabi), Saudi Arabia, Qatar, Belgium, Singapore, and across Europe including Paris, Frankfurt, Amsterdam, Zurich, Dublin, and beyond. Wherever you are based, the ITIN certification process can be completed via a video call if original documents are sent to one of our representative offices.

Full details of the CAA certification process and what to expect step by step are available on the ITINCAA website.

If you are completing your own Form W-7 application before approaching a CAA, our ITIN Form W-7 application guide and ITIN application checklist cover the most common errors and how to avoid them.

Questions We Are Asked Most Often About the 2022 Refund Deadline

Can the IRS actually keep my refund if I miss the deadline?

Yes. Section 6511 of the Internal Revenue Code is enforced strictly. Once the three-year window closes, the IRS has no legal obligation to return the funds, and the courts have upheld this rule repeatedly. There is no mechanism to appeal a missed refund deadline in ordinary circumstances.

I received a 1042-S for 2022 but I did not know I had to file. Does that help?

Unfortunately not. Lack of awareness does not extend the three-year statute. The IRS does not issue penalties for failing to claim a refund — they simply keep the money. The only remedy is to file before the deadline.

What if I both owe tax and have a refund from withholding?

This is a reason to seek professional advice, not a reason to avoid filing. In most cases involving excess withholding on Forms 1042-S, 8805, or 8288-A, the refundable amount significantly exceeds any liability once the return is correctly prepared. Filing late may attract penalties on any balance owed, but refund-only filings do not carry late-filing penalties.

I am based in the UK and want to claim US tax refunds. How does that work?

The UK-US tax treaty is one of the most comprehensive bilateral agreements in the US treaty network. It covers investment income, gambling winnings, and other categories at significantly reduced withholding rates. UK residents filing 1040-NR returns can claim the treaty position and recover excess withholding. Our US tax refund reclaim service for UK-based clients covers how this works in practice.

Do I need an ITIN if I am applying as the non-US spouse of a US citizen?

Yes. If a US citizen or green card holder wants to file a joint 1040 using Married Filing Jointly status and their spouse does not have a Social Security Number, the non-US spouse must obtain an ITIN. The same applies if a non-US spouse is being claimed as a dependent on a US return. This is one of the most frequent ITIN application scenarios our team handles, and it can be completed fully via a CAA without sending the original passport to the IRS.

I am a foreign partner in a US LLC. I have never filed anything. What are my obligations?

Foreign partners receiving Schedule K-1 and Form 8805 each year have a US tax filing obligation. If withholding is shown on those forms, a 1040-NR return can be filed to reclaim the excess. If you have never filed, the 2022 tax year refund window closes on 15 April 2026. See the full guide to ITINs and filing for foreign partners in US LLPs and LLCs for the detail.

Can I file from India, UAE, Singapore, or anywhere outside the US?

Yes. Non-residents file from outside the US regularly. The return and any ITIN application are submitted by post to the IRS ITIN office. Working with an IRS U.S. Tax Service simplifies the document certification and submission process significantly, wherever you are based.

Where do I send the return and ITIN application?

The correct mailing address depends on whether you are including an ITIN application with your return. Our post covering mailing addresses for 1040 and 1040-NR returns submitted with ITIN applications provides the current IRS addresses and guidance on what to include in each submission.

How Our Team Helps You File Before the Deadline

Our team comprises IRS-approved U.S. Tax Services, and UK-qualified tax professionals with experience across Association of Taxation Technicians (ATT), Association of Accounting Technicians (AAT), and Big 4 backgrounds. We handle the complete 2022 filing process end to end.

The scope of our service covers:

- Review of your 2022 withholding forms — 1042-S, 1099, 8805, 8288-A, K-1, and W-2G

- Preparation of the 1040-NR or 1040 US tax return with correct treaty positions applied

- New ITIN application or ITIN renewal via Form W-7, where required

- Passport and identity document certification by our IRS-approved CAA team (no original documents sent to the IRS)

- Submission of the complete package to the IRS ITIN office by tracked post

- Follow-up on ITIN application status using our dedicated CAA phone line

- Handling of any CP566 or CP567 rejection notices, with re-submission at no additional cost up to three attempts

We work on a fixed fee agreed in advance. Identity verification is conducted via video call, which means clients in London, Manchester, Edinburgh, Birmingham, Bristol, Dublin, Paris, Frankfurt, Amsterdam, Dubai, Abu Dhabi, Bangalore, Chennai, Mumbai, Singapore, and anywhere else can complete the full process without travel.

Full details of both the US tax filing and ITIN services are available through Tax and Accounting Hub and ITINCAA.com.

The Deadline Will Not Move. The Refund Will Not Wait.

15 April 2026 is not a target date to revisit when things quieten down. The preparation of a 1040-NR return, ITIN application, document certification, and postal submission to the IRS takes time. The IRS itself takes time to process applications once received.

If you received a Form 1042-S, Form 1099, Form 8805, or Form 8288-A for the 2022 tax year and have not yet filed, contact our team today. We will confirm whether a refund is available, prepare the return, and handle the complete submission so that you do not lose what you are legitimately owed. Reach us through Tax and Accounting Hub or ITINCAA.com.